Tom Willis is an award-winning marketing leader and Co-founder of Lawpath. Tom’s journey journey includes steering several entrepreneurial projects and addressing the unique challenges faced by small businesses. As the Chief Marketing Officer at Lawpath, Tom has been pivotal in shaping the company’s marketing strategy and business growth.

115,949 new businesses were registered in Australia in February 2026. In most years, the month after January is where the energy drops off. Registrations ease. Momentum fades. The numbers return to normal. That did not happen this February.

Growth accelerated. Company formations surged. A state not usually associated with startup activity posted the fastest growth in the country. And one industry expanded at a rate that has no real comparison in recent index history.

The February 2026 Lawpath Business Index draws on verified data from the Australian Business Register and ASIC, combined with anonymised insights from thousands of registrations processed through the Lawpath platform. Together, they give a timely, ground-level view of how Australian entrepreneurship is actually behaving.

This month, the defining theme is acceleration. The businesses being formed in February are not simply a continuation of January’s wave. They represent a broadening of it, across age groups, geographies, industries, and structural choices that show founders entering the market with growing confidence and clear purpose.

For business owners already operating, the February numbers carry a specific message: the new competitive activity entering your market is not uniform, and understanding where it is coming from matters more than simply knowing how much of it there is.

Table of Contents

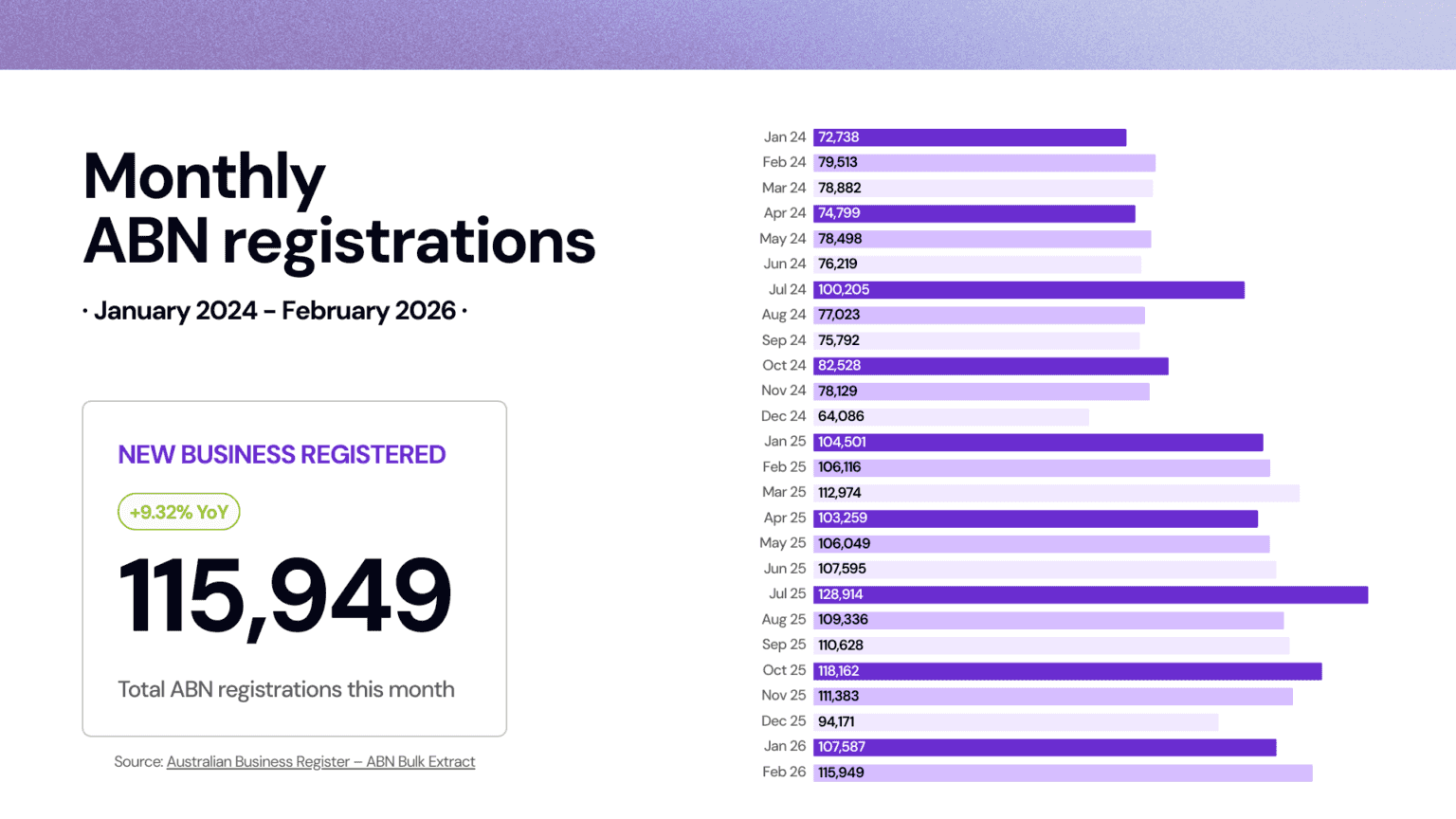

Monthly ABN Registrations

February 2026 recorded 115,949 ABN registrations, a 9.32% increase year on year from 106,061 in February 2025. That rate of growth is more than three times January’s 2.9% year-on-year figure, a sharp acceleration rather than a gradual drift upward.

To register 115,949 ABNs across a 28-day month means Australia was formalising roughly 4,141 new businesses every single day in February. That is not a market running hot at the margins. It is a market operating at a level that would have been exceptional by any recent standard.

What this growth rate signals, more than the raw volume, is that the January registration surge was not a one-month event driven by new year motivation. Founders who did not move in January moved in February, and they did so at a faster pace.

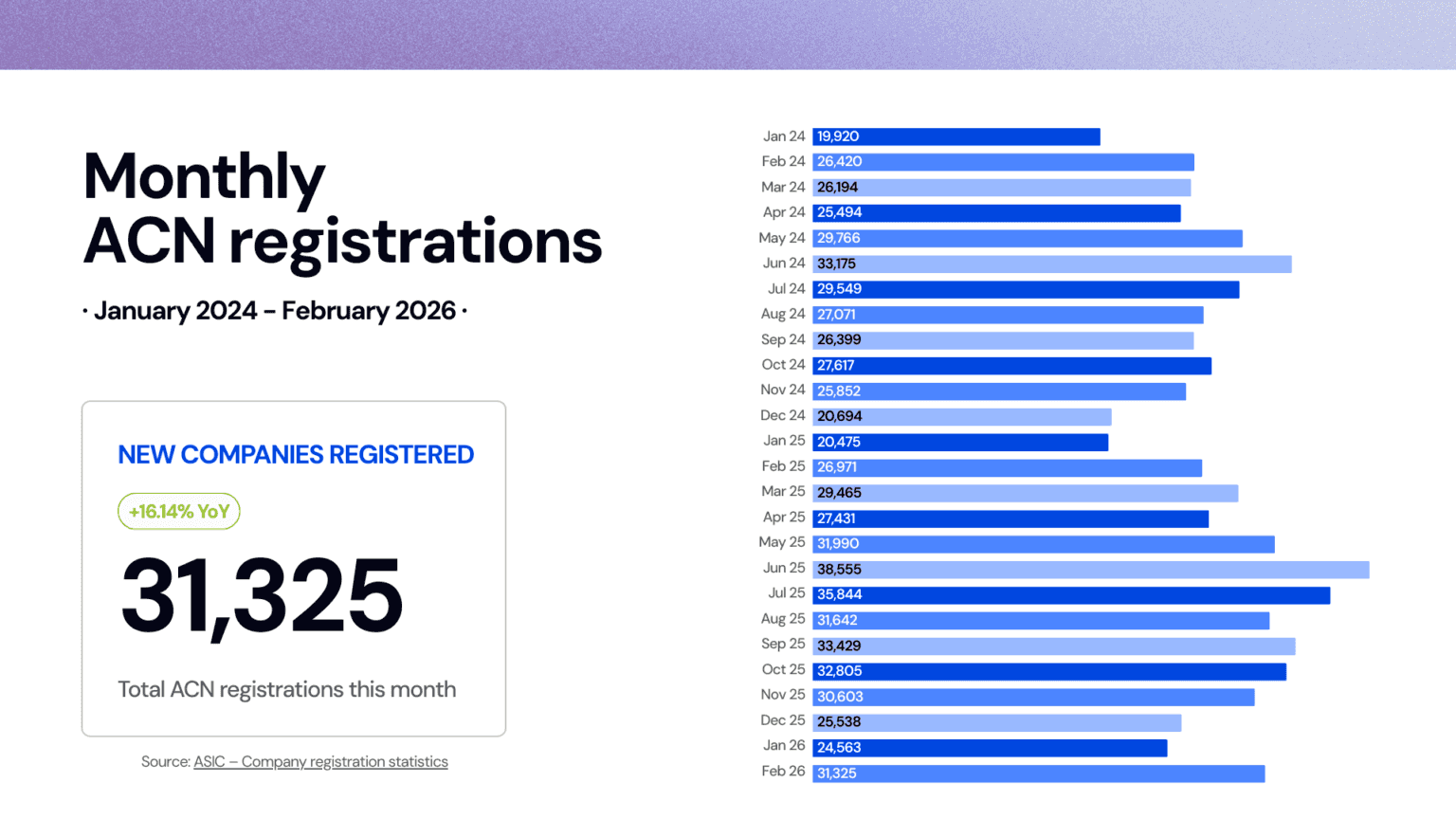

Monthly ACN Registrations

Company formations in February delivered the strongest result in the index this year. 31,325 new companies were registered, up 16.14% year on year from 26,971 in February 2025, and a significant increase from January’s 24,563.

The gap between ABN growth (9.32%) and ACN growth (16.14%) is the key detail. Company formations are not simply following the general market upward. They are running well ahead of it. Founders are actively choosing corporate structures at a rate that outpaces the broader formation trend.

This is a different picture from the structure-first, trade-later pattern noted in January. February’s ACN figures suggest a cohort that is not only incorporating early but doing so as part of a broader move toward commercially active intent, a pipeline that appears to be filling faster than it empties.

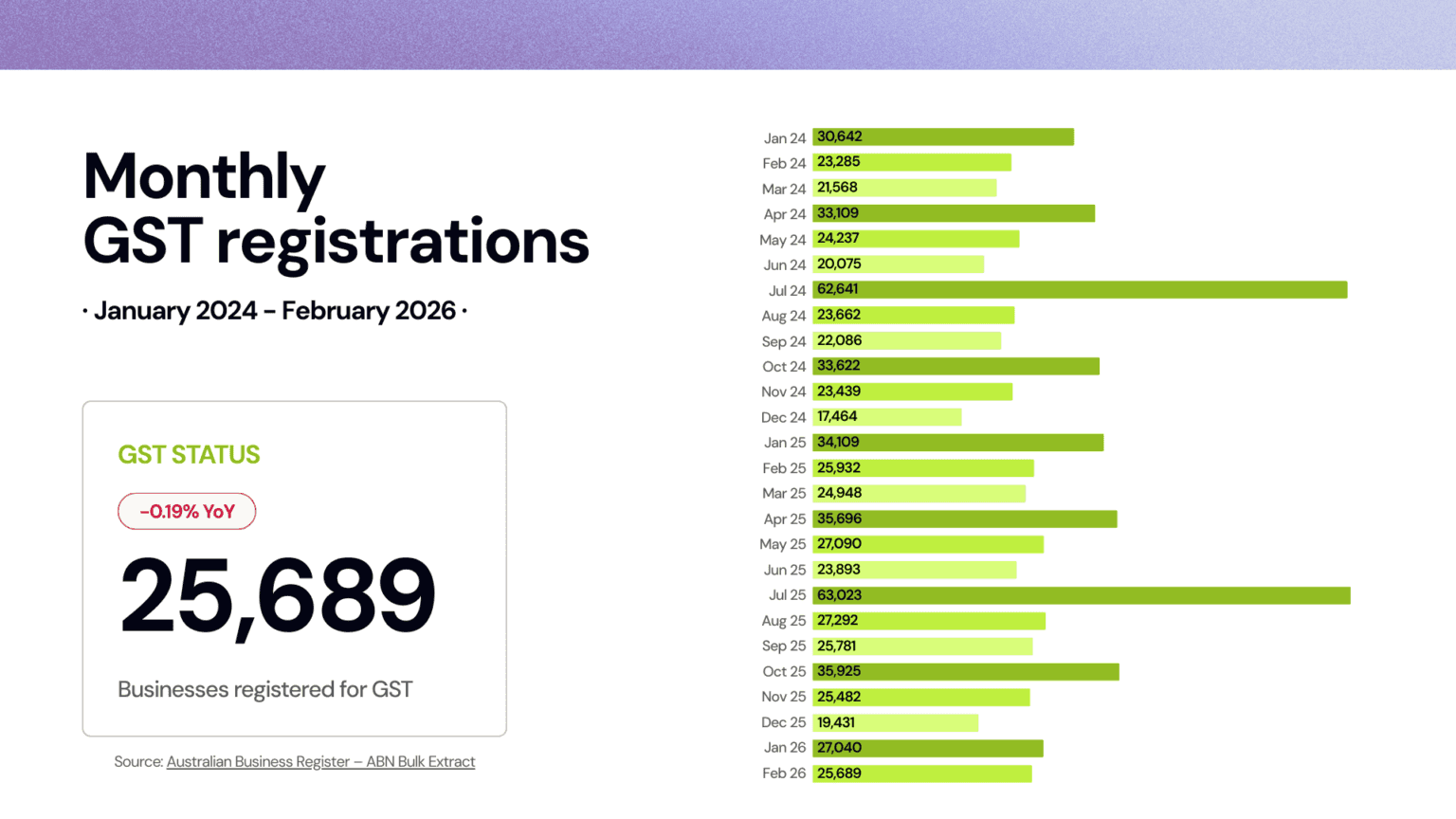

Monthly GST Registrations

25,689 businesses registered for GST in February, representing a near-flat change of -0.19% year on year from 25,738 in February 2025.

The contrast with January is worth noting. January recorded a steep 20.72% year-on-year GST decline. February’s figure is effectively unchanged from the prior year, a near-complete reversal of that pattern in a single month. The gap between ABN growth and GST registrations has narrowed noticeably, suggesting that February’s founders skew more toward active, revenue-generating businesses than the January wave.

This does not mean the market has fully closed the gap between business formation and tax activation. Many new operators are still trading below the $75,000 threshold or choosing to delay registration until their revenue picture is clearer. But the near-stabilisation of GST registrations alongside accelerating ABN and ACN growth is a materially different signal than January produced.

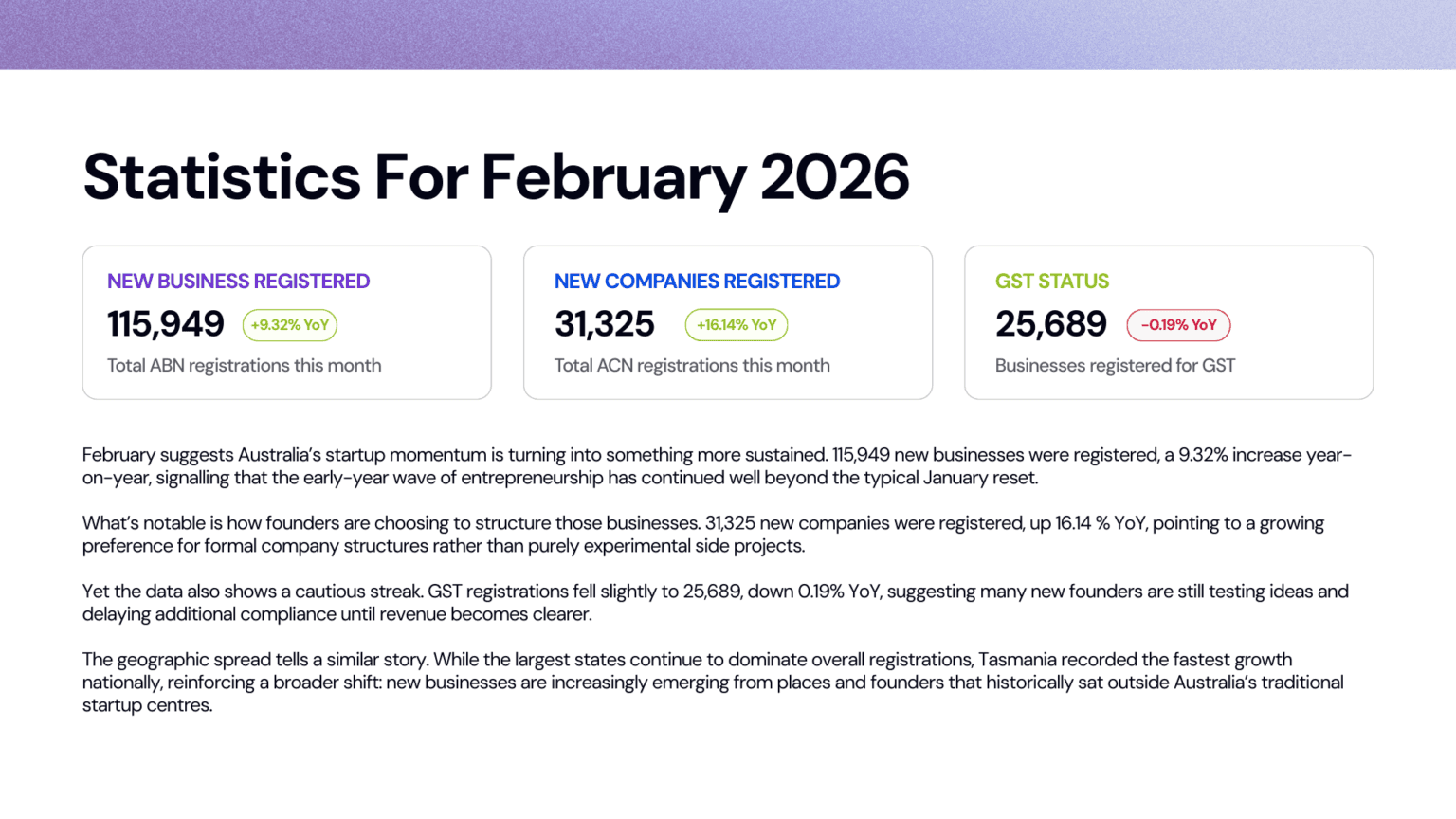

Statistics for February 2026

The three headline figures for February tell a clear and distinct story.

ABN registrations grew at their fastest year-on-year rate in recent months. ACN registrations accelerated even more sharply. And GST registrations, which fell heavily in January, returned almost exactly to prior year levels.

This combination reflects a market that is maturing quickly. January’s founders were cautious entrants testing the water. February’s founders are arriving with more structure, more revenue readiness, and more willingness to formalise their tax position. The cautious streak has not disappeared, as the GST-to-ABN gap remains real, but it has narrowed in a way that points to growing commercial confidence across the cohort.

Against a backdrop of persistent cost-of-living pressures and a labour market in transition, February’s data suggests that entrepreneurship is functioning as more than a fallback. For a growing number of Australians, it is becoming the primary plan.

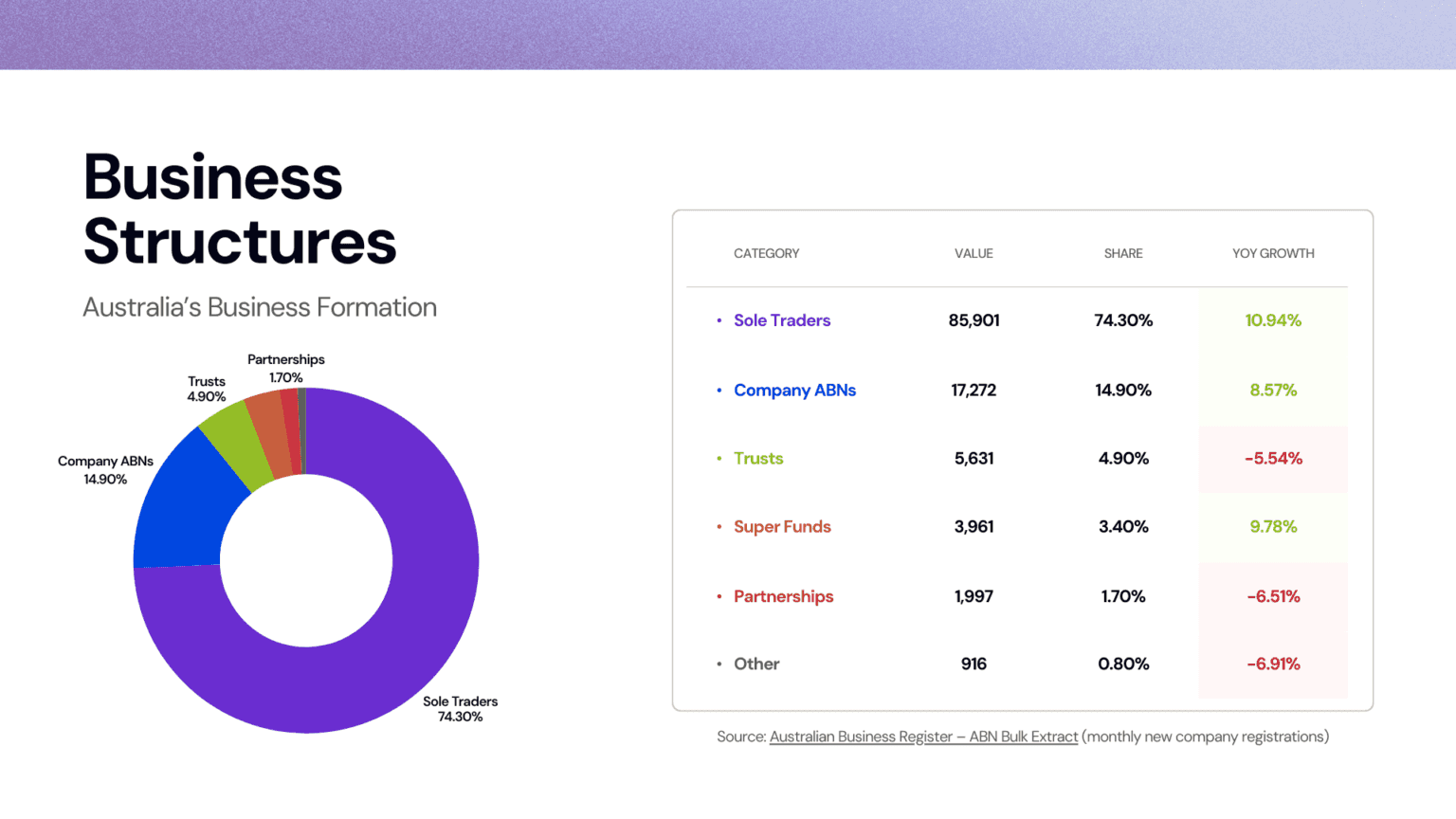

Business Structures

Sole traders accounted for 85,901 registrations in February, the dominant structure by volume, and one that posted 11% year-on-year growth, a clear step up from January’s 4.66%. The sole trader model’s appeal has not changed: fast to set up, simple to run, and immediately responsive to income opportunity. The acceleration in this segment suggests more Australians are formalising existing income activity rather than waiting for the right moment.

The structural story of February, though, belongs to companies. With 31,325 new ACNs growing at 16.14% year on year, nearly double the ABN growth rate, incorporation is clearly the faster-moving segment. This is not the same pattern flagged in January, where company formation growth was partly linked to non-trading entities and structural preparation. February’s ACN momentum, alongside a near-stabilisation in GST registrations, points more directly toward founders building active commercial entities from the start.

A few key dynamics are shaping this shift:

- Revenue-ready incorporation: February’s founders are increasingly incorporating at the point of commercial activation, not simply as preparation, which is consistent with the improvement in GST registration rates.

- Post-January pipeline conversion: Some of January’s elevated company formations appear to be moving toward active ABN registration and trading, contributing to February’s ABN acceleration.

- Experienced founders choosing structure early: The dominant demographic shift in February, toward the 45 to 54 age group, likely influences structure choice. More experienced founders tend not to default to sole trader arrangements.

- Scalability from day one: Founders in high-growth sectors, particularly personal services and digital businesses, are structuring for growth from the outset rather than retrofitting governance later.

Whether this structural confidence holds through the quieter mid-year months will be the key question the March and April data will need to answer.

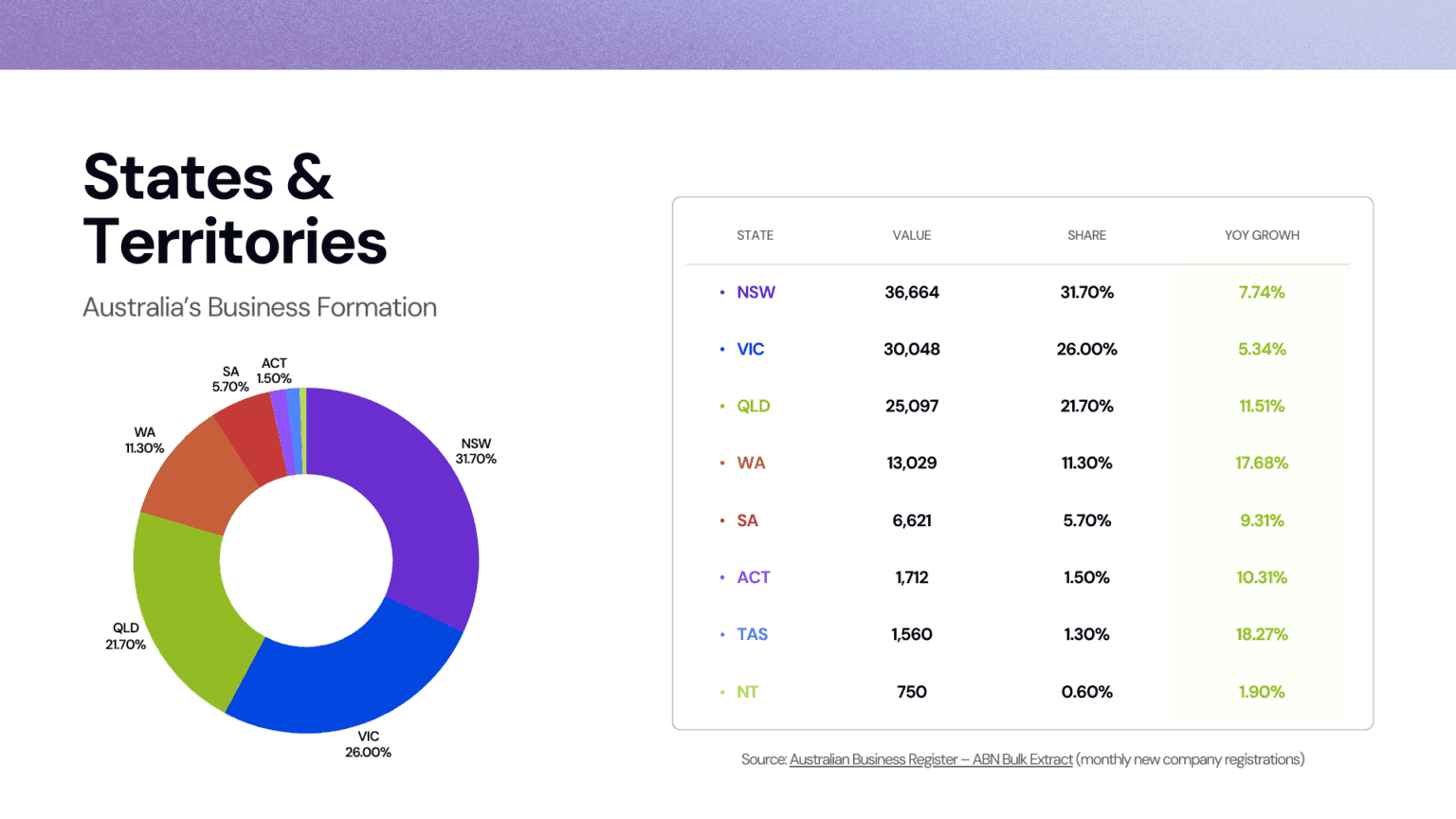

States and Territories

New South Wales, Victoria, and Queensland continue to generate the highest absolute registration volumes, reflecting their combined population size and established commercial infrastructure. This is unlikely to shift in the near term.

What February added was a clear growth standout: Tasmania recorded the fastest year-on-year growth of any state or territory in the country at 18%. That is not a statistical quirk of a small base. It is a genuine sign of accelerating entrepreneurial activity in a market that has historically sat well outside Australia’s startup conversation.

The drivers are familiar but no less significant: relative affordability, inward migration, and the continued growth of remote-enabled work as a viable operating model. Tasmania’s emergence as the growth leader in February is the clearest sign yet that Australia’s entrepreneurial geography is being redrawn well beyond the traditional capitals.

Western Australia, South Australia, and the Northern Territory continue their steady contribution to this decentralisation, reinforcing that business formation is spreading across the country rather than concentrating further in established centres.

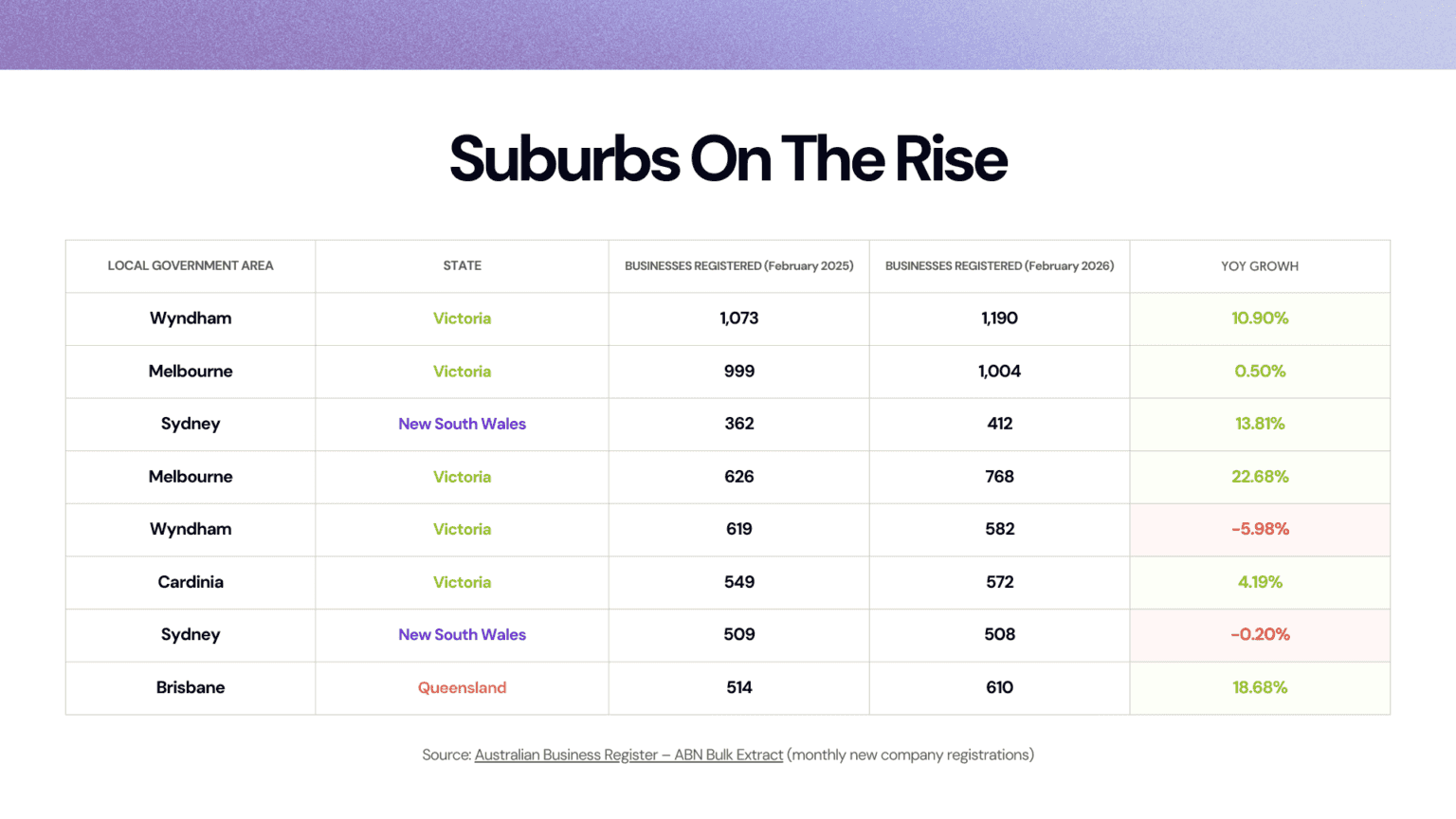

Top Suburbs by New Business Registrations

Sydney, Melbourne, and Brisbane CBDs continue to record the highest registration volumes, supported by professional density, infrastructure, and the network effects that come with established commercial hubs. That positioning remains durable.

The more telling number in February is postcode 3029, covering Hoppers Crossing and Wyndham Vale in Melbourne’s outer west, which recorded 1,190 new registrations and the highest single suburb volume in the index. This is not a professional services corridor or an inner-city startup precinct. It is a fast-growing outer metro community where population growth has created demand that existing businesses have not yet caught up to.

The presence of a suburb like 3029 near the top of the volume rankings is a clear signal about where commercial opportunity is forming and where it may be underserved.

Suburbs Experiencing Rapid Growth

Percentage-based growth in February is concentrated in suburban and peri-urban locations across Tasmania, Queensland, outer Western Australia, and regional South Australia.

These are communities in demographic transition, growing faster than their service infrastructure, creating demand-driven conditions where new businesses are not entering a crowded market but filling genuine gaps. For established operators considering expansion, these are not speculative bets. They are markets where the population is arriving ahead of the competition.

The window of relatively low competition in these corridors will not stay open indefinitely. February’s data suggests founders are starting to notice.

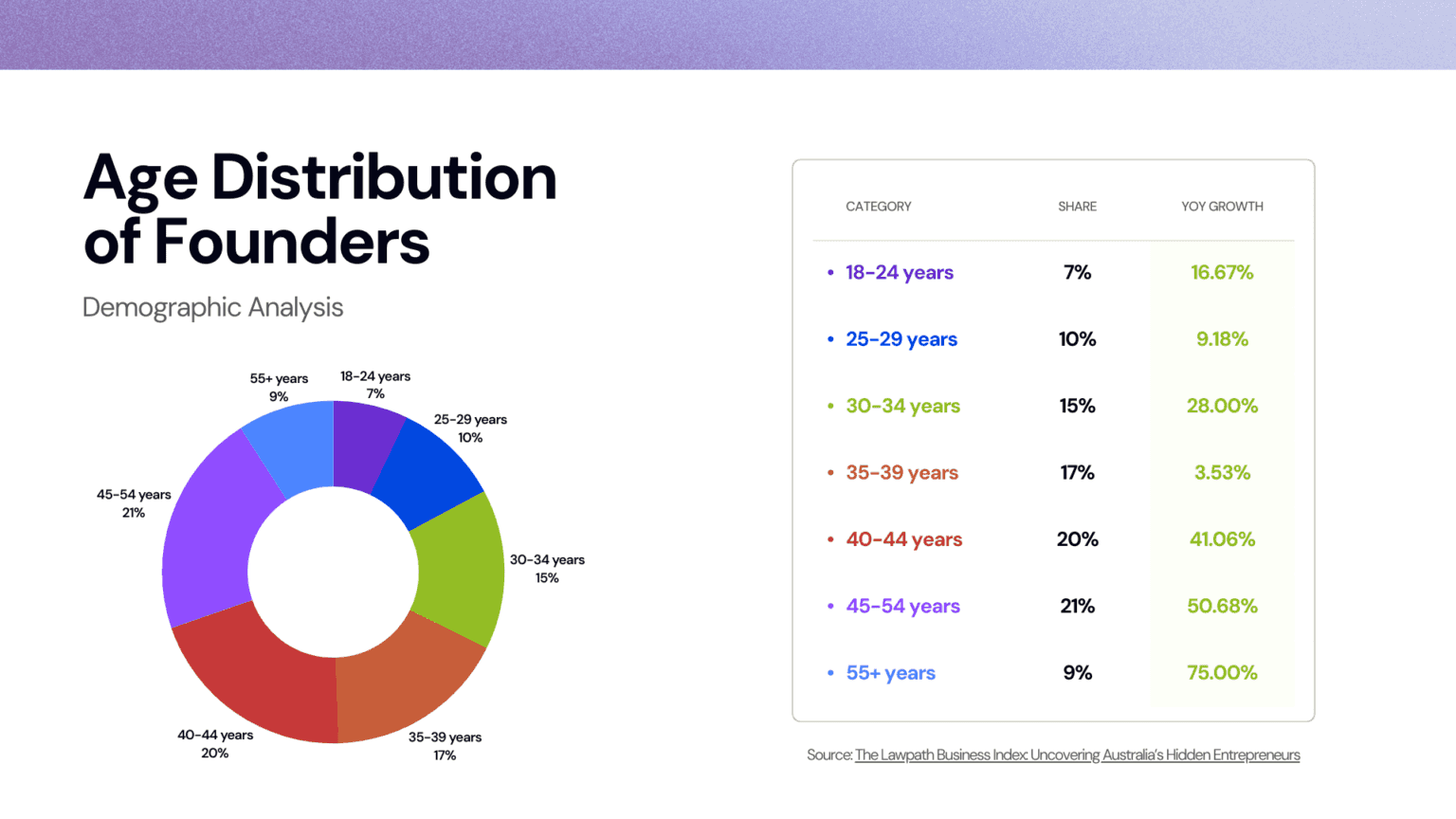

Age Distribution of Founders

The standout demographic shift in February is clear. Founders aged 45 to 54 not only represent the largest share at 21% of all registrations, they also recorded 21% year-on-year growth, the sharpest rise of any age group in the index.

This is a different kind of founder from the one that tends to dominate the entrepreneurship conversation. Mid-career professionals in this cohort typically bring deep industry knowledge, established client relationships, existing capital, and a clear view of the market they are entering. They are not testing a concept. They are putting experience to work.

In a labour market undergoing structural change, with redundancies, role changes, and sector consolidation all contributing to mid-career uncertainty, the 45 to 54 surge likely reflects both opportunity and necessity. Whatever the individual motivation, the outcome is consistent: this cohort tends to build more durable businesses, faster.

Younger founders remain active and visible, and the conditions that support early career entrepreneurship, including low formation costs and accessible digital tools, have not changed. But February’s growth edge belongs to the experienced end of the age spectrum.

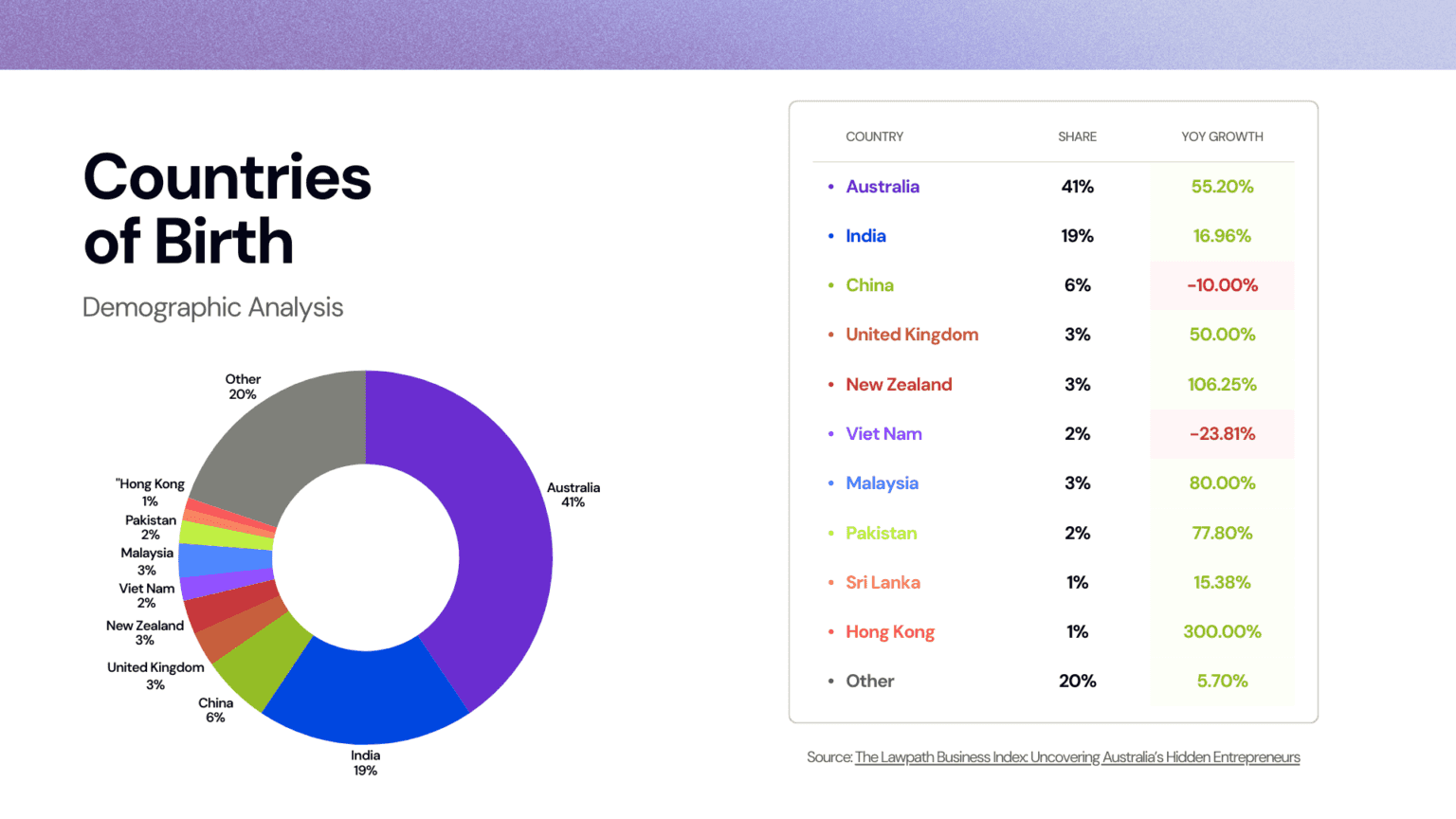

Countries of Birth

February’s platform data presents one of the more striking figures in the index: 59% of founders registered through Lawpath were born outside Australia, with Australian-born founders representing 41% of registrations.

This is not a marginal contribution from a diverse minority. It is a majority. Australia’s entrepreneurial activity is being shaped, by a clear numerical margin, by founders who bring international experience, cross-cultural perspectives, and commercial instincts developed in different markets.

The spread of overseas-born founders is broad, covering many countries of origin. For established businesses, this diversity is both competitive context and a market signal. The communities, consumer behaviours, and spending patterns shaped by Australia’s migrant majority are among the fastest-changing segments of the local market.

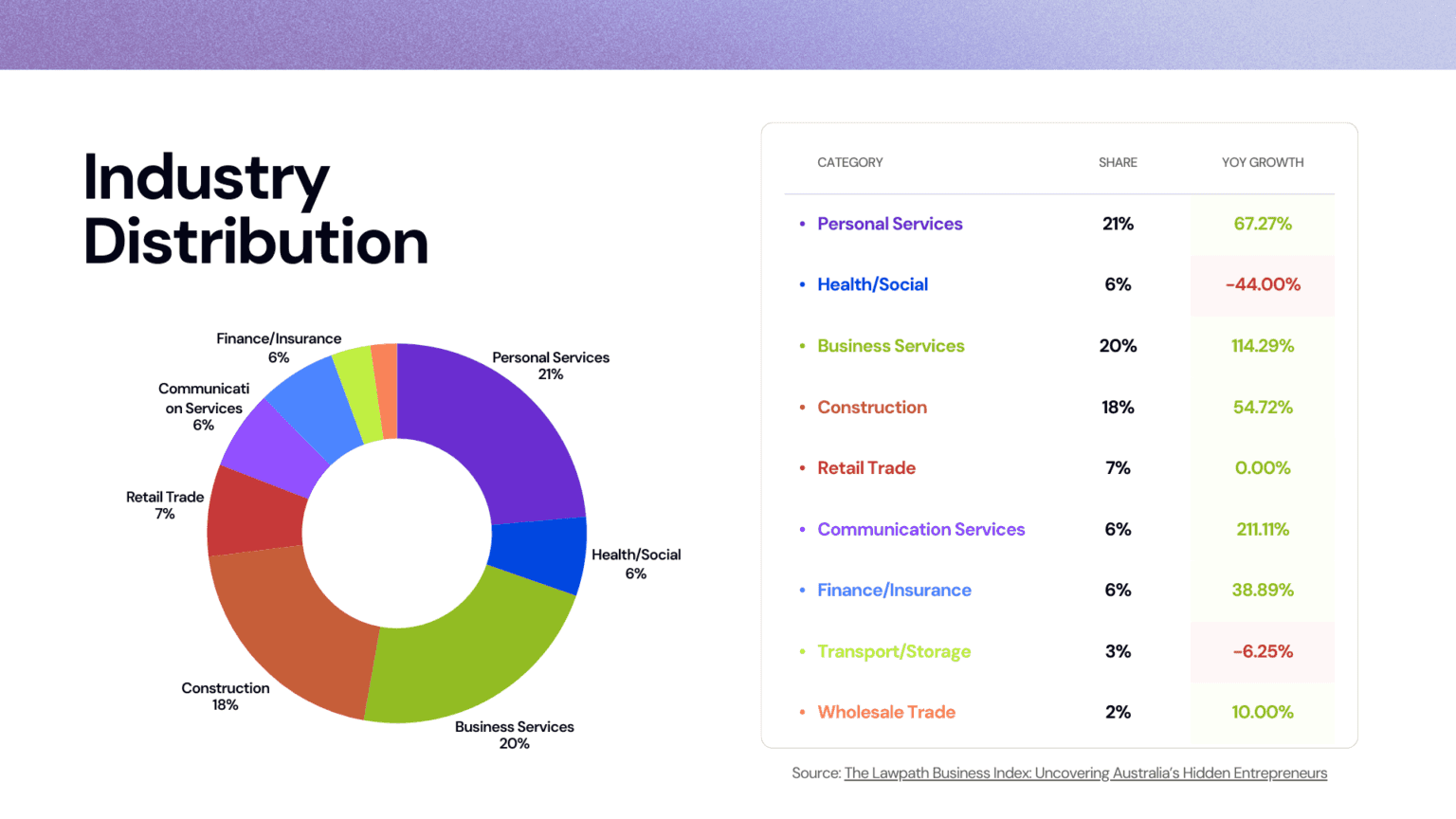

Industry Distribution

The industry story of February belongs to personal services. Representing 21% of all new registrations, it was already the leading sector by share, but its 67% year-on-year growth rate is the number that demands attention.

A 67% surge has no easy comparison in recent index data. It reflects structural demand in a part of the economy where existing supply is running behind what households and individuals are looking for. Whether the drivers are demographic, such as an ageing population requiring more support, or linked to lifestyle changes or the formalisation of previously informal service work, the scale of this growth is large enough to affect pricing, staffing, and competitive positioning for anyone operating in related categories.

Construction trades, professional services, property, transport, and online commerce continue to represent active formation sectors. These are ongoing responses to real economic conditions, not speculative bets.

Why this matters for business owners

February 2026 answers a question that January left open: whether the elevated start to the year would hold, or ease as the calendar moved forward.

It held. 115,949 new businesses, 9.32% year-on-year ABN growth, 16.14% ACN growth, and near-flat GST registrations together describe a market that did not exhaust itself in January. It expanded. And it expanded with a specific character: more experienced founders, faster-growing structures, a geographic spread that now includes Tasmania as the country’s leading growth state, and a single industry in personal services posting growth rates that are reshaping the competitive density of that sector.

For existing businesses, the February data is not background noise. It is a signal about the competitive environment forming around you, covering who is entering, where they are based, how they are structured, and which sectors they are targeting. Understanding those patterns is just as strategically important as understanding your own customers.

The Lawpath Business Index will continue tracking these developments each month, providing the clearest available view of how Australian business is evolving in real time.