Dominic is the CEO of Lawpath, dedicating his days to making legal easier, faster and more accessible to businesses. Dominic is a recognised thought-leader in Australian legal disruption, and was recognised as a winner of the Australian Legal Innovation Index and recently a winner of the LexisNexis 40 Under 40 (APAC).

Tech giant, Facebook and smaller startups are building software to make it easier for banks to assess your credit risk based on your social media presence.

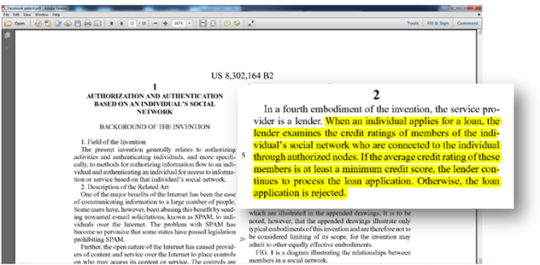

Earlier this month, Facebook was granted an updated patent for a method of authentication based on your Facebook friends. Increasing our privacy and avoiding spam, what a noble goal. However, Facebook now also owns a mechanism to assess credit applications based on the individual’s social network.

Although Facebook will likely not use the patent any time soon, it certainly highlights new mechanisms lenders employ to assess credit risk, especially in the absence of a credit history. Banks in 39 countries now incorporate Facebook data to assess applicants’ credit risks although Australian banks shy away from disclosing whether they use this method.

‘876 Facebook friends’ – must be rich

US startups’ have further developed new ways of determining someone’s credit risk. Lenddo, for example, examines whether you are friends on Facebook with someone guilty of late repayments and how close you are based on your interactions. Its analysis is premised on the belief that if your friends have defaulted, so will you.

LendUp, another startup, offers loans assessing applicants via an algorithm that scans Facebook to verify both the information you have provided and to assess your social life as an indicator of stability. According to Orloff, co-founder and CEO of LendUp, “If you have a very strong, close geographic network, that’s helpful to you” because it demonstrates that you have a support base.

The effectiveness of these techniques has been met with scepticism. John Ulzheimer, a credit expert, says they are not necessarily indicative of credit risk. However, if community banking has been replaced with online or corporate banking, then lenders’ examination of your online persona may not be so alien after all. The local banker would have known about your family life, your number of children, the health of your business and your support network, before accepting a loan application.

Location, location, location

Lenders may also consider your area of residence to assess your credit risk. A study, reported last week in the Financial Review, listed the top postcodes most at risk of mortgage default. What suburbs would you predict on the list? Perhaps Western Sydney households or the outer suburbs of Melbourne.

The study reported that, although those predicted areas featured, the suburbs most at risk of defaulting were those that would not be able to maintain payments in cases of unforeseen circumstances like an increase in interest rates and unemployment. In particular, rural and isolated regions were most at risk because finding alternative employment would be more difficult than in the city.

Can I afford to borrow?

Remember that to borrow is to spend. When you borrow you are required to pay interest and risk losing your secured assets if you default. Weigh up therefore, whether you could wait and save to avoid the additional cost. You should also assess whether your current budget leaves room for the extra expenses.

It may be the right time for you to borrow. You may foresee a steady income, perhaps even a promotion. Your credit risk may currently allow you to secure a sound deal with low interest rates and fair terms. After all, you do live in Paddington with all your 876 Facebook friends!

If you are ready to borrow or lend money, with LawPath you can now create a Loan Agreement (Lender to Borrower) or Loan Agreement (Borrower to Lender) in under 10 minutes.

Unsure where to start? Contact a LawPath consultant on 1800LAWPATH to learn more about customising legal documents, obtaining a fixed-fee quote from one our network of 600+ expert lawyers or any other legal needs.